Understanding Your Partnership Firm's Tax Duties

Under the Income Tax Act, 1961:

- A partnership firm is subject to a flat tax rate of 30% on its profits.

- A 12% surcharge is levied when the firm’s taxable income exceeds Rs. 1 crore.

- A 4% health and education cess is also applicable to firms.

Note: Unlike individuals or Hindu Undivided Families (HUFs), no basic exemption limit applies to partnership firms. Tax is levied on the entire taxable income.

Why must You File a Tax Return Even with No Profit (Nil Income)?

Even if a partnership firm has no profit (or even a loss) in a financial year, filing an Income Tax Return (ITR) is mandatory in India.

1. Legal Obligation: Under the Income Tax Act, 1961, every partnership firm (whether registered or unregistered) is considered a separate taxable entity and is legally obligated to file an ITR (Form ITR-5) annually, regardless of its income or loss position. Failing to do so is a non-compliance.

2. Electronic Filing Requirement: Form ITR-5 must be filed electronically through the Income Tax e-filing portal. If the firm is subject to a tax audit, filing must be done using a Digital Signature Certificate (DSC).

3. Carry Forward of Losses: This is a crucial benefit. If your firm incurs a loss in a financial year, you can only carry forward these losses to offset against future profits and reduce your tax liability in subsequent years if you file your ITR by the due date. If you don’t file, you lose the ability to carry forward most types of losses (e.g., business loss, capital loss).

Example: Suppose your partnership firm reports a business loss of Rs. 2.5 lakhs in FY 2024–25. If you file your ITR on time, you can carry forward this Rs. 2.5 lakhs and adjust it against future profits in the next 8 years, reducing future tax burdens. However, if you fail to file the return, you lose this right, and the entire loss lapses.

4. Avoid Penalties and Consequences:

- Late Filing Fees: Even for a NIL return, a late filing fee of Rs. 5,000 is levied under Section 234F. However, if the firm’s total income is Rs. 5 lakh or less, the fee is reduced to Rs. 1,000.

- Interest: If any tax was due (even if calculated to be zero after deductions but before filing), interest under Section 234A might be charged.

- Prosecution: In severe cases of non-compliance, particularly if there’s a history of not filing, which could be viewed as tax evasion, or if the tax liability (even if unpaid) was substantial, the firm and its partners could face prosecution.

- Operational and Reputational Impact: Not filing can lead to a negative standing with tax authorities, potentially affecting other aspects of the firm’s operations.

5. Proof of Financial History: ITRs serve as official proof of the firm’s financial activities. This is invaluable for:

- Loan Applications: Banks and financial institutions often require ITRs for the past few years when applying for business loans, overdraft facilities, or even personal loans for partners.

- Visa Applications: When partners apply for international visas, embassies often request ITRs as proof of financial stability.

- Tender Applications: For bidding on government or private tenders, consistent ITR filing demonstrates compliance and financial transparency.

6. Claiming Refunds: If the firm had any Tax Deducted at Source (TDS) on its income (e.g., on interest received, or payments from clients), even if no final tax was payable, you can only claim a refund of this TDS by filing the ITR.

7. Maintaining Records and Transparency: Filing the ITR ensures that the firm maintains accurate financial records, which are essential for good governance, internal transparency among partners, and future financial analysis.

Which ITR Form to Use for a Partnership Firm?

ITR-5 is used by most partnership firms. Non-LLP firms under presumptive taxation can use ITR-4 if the income is within Rs. 50 lakh, and an audit isn’t required.

Regardless of profit or loss, filing the ITR is legally mandatory for a partnership firm, usually via ITR-5, to fulfill compliance, carry forward losses, and avoid penalties.

ITR-5: Main form for partnership firms

ITR-5 is the primary Income Tax Return form mandated for most partnership firms in India. This form is specifically designed for entities such as:

- Partnership Firms (both registered and unregistered)

- Limited Liability Partnerships (LLPs)

- Association of Persons (AOPs)

- Body of Individuals (BOIs)

- Artificial Juridical Persons (AJPs)

- Cooperative Societies

- Local Authorities

- Estates of deceased persons or insolvents

- Business Trusts and Investment Funds

It is crucial to note that ITR-5 is for the firm itself and not for the individual partners. The firm is required to file ITR-5 electronically, andif the firm is subject to an audit, a Digital Signature Certificate (DSC) is mandatory for verification.

When can a Partnership Firm use ITR-4 (Sugam)?

A partnership firm (excluding LLPs) can file ITR-4 (Sugam) only if it opts for the presumptive taxation scheme, which is entirely optional. To be eligible, the firm must meet the following conditions:

- Presumptive Taxation: The firm must opt for the presumptive taxation scheme under Section 44AD (for eligible businesses), Section 44ADA (for eligible professionals), or Section 44AE (for those engaged in the business of plying, hiring, or leasing goods carriages).

- Total Income Limit: The firm’s total income should not exceed Rs. 50 Lakh during the financial year.

- No Audit Requirement: Generally, firms opting for presumptive taxation under ITR-4 are not required to maintain detailed books of accounts or get their accounts audited, provided they declare income at the prescribed presumptive rates. However, if their actual income is lower than the presumptive income and they wish to declare the lower income, they would need to maintain books of accounts and get them audited, which would then make them ineligible for ITR-4 and require ITR-5.

- No Complex Income: The firm should not have income from sources like capital gains (with minor exceptions for certain LTCG up to Rs. 1.25 lakhs under Section 112A with no brought-forward losses), more than one house property, lottery winnings, or foreign assets.

Firms must carefully assess eligibility before opting for ITR-4. Incorrect filing can lead to compliance issues and penalties.

Due Dates for Filing Partnership Tax Return (AY 2025-26)

Filing the Income Tax Return (ITR) on time is crucial for partnership firms to remain compliant, avoid penalties, and avail benefits like carry forward of losses. The due dates vary based on whether the firm is subject to audit or transfer pricing provisions.

Notes:

- The original due date for non-audit cases was July 31, 2025, which has been extended to September 15, 2025, by the CBDT.

- The Financial Year (FY) for AY 2025-26 is April 1, 2024, to March 31, 2025.

- Failing to file the return by the due date may attract penalties and interest under the Income Tax Act, 1961.

- These dates are subject to change if the CBDT issues an extension. Always verify the current deadlines on the official portal.

What Happens If You Don’t File Your Partnership ITR?

Failing to file your Income Tax Return (ITR) can lead to several severe consequences, including penalties, interest, and legal action.

Here are the key repercussions you might face:

What to do if ITR Filing is Missed?

If you’re concerned about missing the ITR filing deadline, there are still avenues to submit your return:

Belated Return

- If you miss the ITR filing due date, you can file a return after the due date, called a belated return.

- However, filing a belated return means you will be subject to a late fee and interest charges. Additionally, you will forfeit the ability to carry forward any losses for future adjustments.

- Despite this, you are still permitted to claim applicable deductions and exemptions.

- The final date for filing a belated return is December 31st of the relevant assessment year (unless an extension is officially granted by the government).

Updated Return

Even if you miss the December 31st deadline, you may still have the option to file an updated return (ITR-U), provided you meet specific conditions.

What is the Cost of Filing a Partnership Tax Return?

The cost of filing a Partnership Tax Return in India involves both government-mandated taxes and potential late fees, as well as professional charges if you opt for expert assistance.

A. Government Fees and Late Payment Charges

Filing a partnership tax return (ITR-5) in India itself does not involve a direct “government fee” for the act of filing if done within the due date. The government charges are related to the tax liability of the firm and penalties/interest if the filing or payment is delayed.

Tax Liability: Partnership firms are taxed at a flat rate of 30% on their taxable income. A surcharge of 12% applies if the taxable income exceeds Rs. 1 crore. Additionally, a 4% Health and Education Cess is levied on the total tax amount (including surcharge). Partnership firms are also subject to Alternative Minimum Tax (AMT) at 18.5% of adjusted total income.

Alternative Minimum Tax (AMT):

- AMT is charged at 18.5% of adjusted total income.

- Applicability: AMT applies only if the firm claims deductions under:

- Chapter VI-A (Sections 80-IA to 80RRB, excluding 80P)

- Section 10AA (for SEZ units)

- AMT does not apply to every firm, especially those not claiming such deductions.

Late Filing Fee (Section 234F):

- If the return is filed after the due date but on or before December 31st of the assessment year, a late fee of Rs. 5,000 is applicable.

- If the total income of the partnership firm is Rs. 5 lakh or less, the late fee is capped at Rs. 1,000.

Interest on Late Payment (Section 234A): If there is any unpaid tax amount, interest at a rate of 1% per month or part of a month is charged on the unpaid tax from the due date until the payment is made.

B. Professional Fees for Filing Your ITR

The cost of filing a partnership tax return through a professional (like a Chartered Accountant service or an online tax filing platform) can vary significantly based on the complexity of the firm’s financial transactions, turnover, and whether a tax audit is required.

Online Platforms: Basic partnership firm filing services on online platforms might start from around Rs. 4,000 – Rs. 6,000, especially for firms not requiring a tax audit.

Chartered Accountants (CAs): CA fees are generally higher due to personalized service, detailed advice, and handling of complex scenarios.

- For a standard partnership firm ITR filing without an audit, fees could range from Rs. 5,000 to Rs. 10,000 or more.

- If a tax audit is mandatory (e.g., if the firm’s turnover exceeds Rs. 1 crore for businesses or Rs. 50 lakh for professionals), the professional fees will be substantially higher, as it involves a detailed examination of accounts and preparation of the Tax Audit Report (Form 3CD). These charges can range from Rs. 15,000 to Rs. 50,000 or even more, depending on the turnover and complexity of the books.

Factors Influencing Fees

The fees charged by Chartered Accountants (CAs) or accounting professionals can vary significantly based on multiple factors. Understanding these variables can help businesses and professionals better estimate their accounting costs and choose the right service provider.

- Turnover/Gross Receipts: Higher turnover generally means more complex accounting and higher fees.

- Number of Transactions: A large volume of transactions can increase the effort required.

- Nature of Business/Profession: Certain industries or professions might have specific compliance requirements.

- Maintenance of Books of Accounts: If the books are not well-maintained, the CA might charge more for reconciliation and preparation.

- Additional Services: Fees may increase if the firm requires other services like GST compliance, TDS compliance, advisory, or balance sheet preparation.

Documents Needed for Filing Partnership ITR

Filing the Income Tax Return (ITR-5) for a partnership firm requires a comprehensive set of documents to ensure accurate reporting of income, expenses, and tax liabilities.

Regardless of whether your firm’s accounts are audited or not, the following documents are crucial for ITR filing:

1. Foundational Documents

These documents show that your partnership firm is officially set up and running. They help identify your firm and make sure it’s eligible for tax filing.

- Partnership Deed: Outlining profit-sharing ratio, roles, and responsibilities of partners

- Partnership Firm Registration Certificate (if registered)

- Udyam Registration Certificate (for MSME classification, if applicable)

- GST Registration Certificate (if the firm is registered under GST)

- ROC Compliance Proof (only if filed mistakenly as LLP; applicable for LLPs, not regular partnership firms)

2. Financial Statements (for the relevant financial year)

These show the financial health of your business during the year.

- Profit & Loss Account: Detailing income and expenses incurred

- Balance Sheet (as of March 31st): Showing assets, liabilities, capital, and current financial position

- Trading Account: For firms involved in the purchase and sale of goods

3. Banking and Accounting Records

These help verify business transactions and support your financial statements.

- Bank Statements: All bank accounts operated by the firm during the year

- Ledger Accounts: Including:

- All heads of income and expenses

- Partners’ capital accounts and drawings

- Loans and advances

- Debtors and creditors

4. Tax-Related Documents

Used to match your tax payments and deductions with government records.

- TDS Certificates (Form 16A, Form 26Q, etc.):

- If TDS is deducted on income received (like professional fees or interest)

- If the firm has deducted TDS on payments made

- Form 26AS / AIS / TIS:

- Consolidated summary of tax deducted, collected, and high-value transactions

- Should be reconciled with the firm’s books

5. Supporting Documents

These add more clarity to the numbers you report in your return.

- Details of Capital Contributions and Drawings: Records of capital introduced and withdrawals by each partner.

- Loan Documents: Details and interest statements for any loans taken or given during the year.

- GST Returns (if applicable): GSTR-1, GSTR-3B, GSTR-9 to match turnover and tax liabilities with ITR.

- Investment Proofs: Details of any investments made by the firm in the financial year.

Additional Documents if Your Firm's Accounts Are Audited

If your partnership firm’s turnover or gross receipts exceed the prescribed limits (currently Rs. 1 crore for businesses or Rs. 50 lakh for professionals, with increased limits for certain cash transactions), a tax audit under Section 44AB is mandatory.

1. Tax Audit Report (Form 3CB and Form 3CD): This report is prepared and certified by a Chartered Accountant.

- Form 3CB: The audit report itself.

- Form 3CD: A statement of particulars that contains detailed information about the firm’s financial activities, compliance with various tax provisions, and disallowances.

2. Detailed Books of Accounts: The auditor will require comprehensive books of accounts, including:

- Cash Book

- Bank Book

- Sales Register

- Purchase Register

- Journal entries

- Ledgers

- Inventory records

- Fixed Asset Register

3. Vouchers and Bills: All original invoices, bills, payment vouchers, and receipts supporting the firm’s income and expenses.

4. Trial Balance: A summary of all ledger balances, used to prepare the final financial statements.

While not directly uploaded with the ITR, these documents are fundamental for the firm’s existence and tax compliance:

Partnership Deed: This legal document outlines the terms and conditions of the partnership, including profit/loss sharing ratios, roles and responsibilities of partners, interest on capital/drawings, and remuneration to partners.

It serves as the governing document and is crucial for calculating partners’ remuneration and interest on capital as per the Income Tax Act. It’s often required by professionals to understand the firm’s structure and valid deductions.

PAN Card of the Partnership Firm: The Permanent Account Number (PAN) is a unique 10-digit alphanumeric identifier issued by the Income Tax Department. The firm needs to conduct any financial transaction, including opening bank accounts, and it is the primary identification for filing its ITR.

PAN and Aadhaar of all Partners: While the ITR is filed for the firm, the details of all partners, including their PAN and Aadhaar numbers, are required in the ITR-5 form.

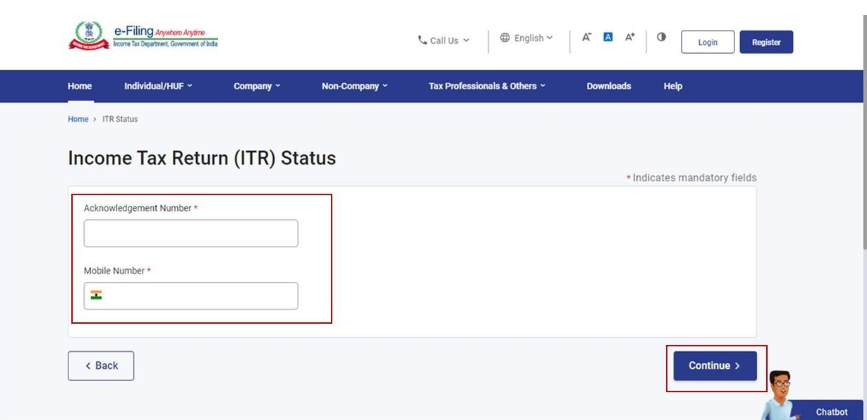

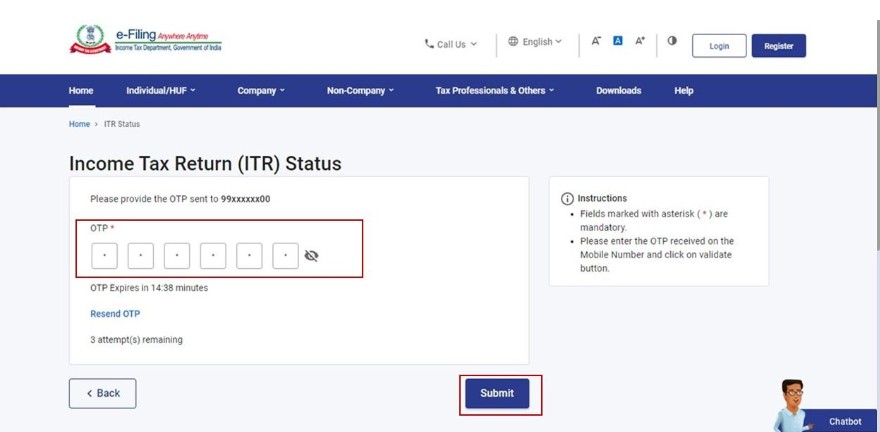

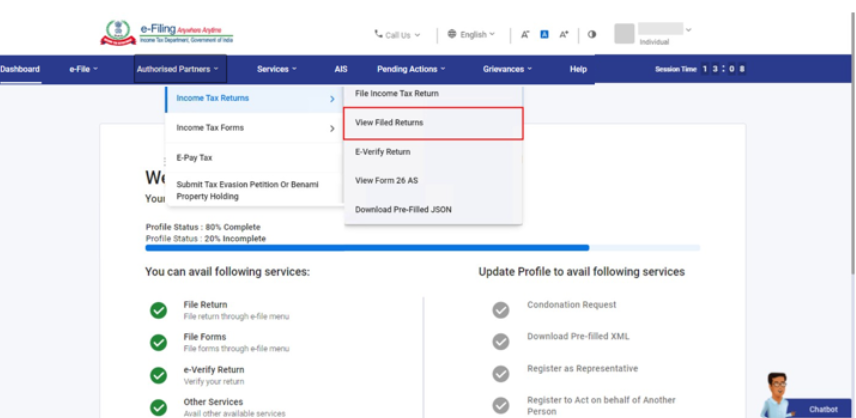

How to File a Partnership Tax Return Online in India?

Filing a Partnership Tax Return (ITR-5) online is mandatory for most partnership firms in India. The process primarily involves preparing your financial data, logging into the Income Tax Department’s e-filing portal, filling out the ITR-5 form, and then verifying it.

Here’s a step-by-step guide on how to file a Partnership Tax Return online:

1. Log in to the Income Tax e-Filing Portal

- Go to the official Income Tax Department e-filing portal: incometax.gov.in

- Login: Use the firm’s PAN as the user ID and enter the password. If you’re a new user, you’ll need to register first.

2. Navigate to "e-File" and select ITR Form

- After logging in, go to the “e-File” menu.

- Select “Income Tax Returns” and then “File Income Tax Return.”

- Select Assessment Year (AY): Choose the relevant Assessment Year (e.g., AY 2025-26 for income earned in FY 2024-25).

- Select Filing Mode: Choose “Online.”

- Select ITR Form: Select “ITR-5.” This is the form specifically for partnership firms (and LLPs, AOPs, BOIs, etc.).

3. Fill in the ITR-5 Form Online

The ITR-5 form is comprehensive and consists of various parts and schedules. You’ll need to fill in the details carefully. The system may pre-fill some information based on your PAN and other data available with the Income Tax Department (e.g., from Form 26AS/AIS/TIS).

- Part A: General Information: Basic details of the firm, nature of business, audit information (if applicable), date of formation, etc.

- Part A-BS: Balance Sheet: Details of assets, liabilities, and partners’ capital as of March 31st of the financial year.

- Part A-P&L: Profit & Loss Account: Revenue from operations, expenses, and net profit/loss for the financial year.

- Part A-OI: Other Information: Details of quantitative particulars, method of accounting, and other relevant information.

- Schedules: These are detailed sections for various types of income, deductions, and tax computations:

- Schedule HP: Income from House Property.

- Schedule BP: Computation of Income from Business or Profession (this is a very important schedule for firms).

- Schedule CG: Capital Gains.

- Schedule OS: Income from Other Sources (e.g., interest income).

- Schedule CYLA: Set-off of current year losses.

- Schedule BFLA: Set-off of unabsorbed losses brought forward from previous years.

- Schedule DPM: Depreciation on Plant and Machinery.

- Schedule DOA: Depreciation on Other Assets.

- Schedule DCG: Deemed Capital Gains on sale of depreciable assets.

- Schedule UD: Unabsorbed Depreciation.

- Schedule CFL: Carry Forward of Losses.

- Schedule 80G, 80GGA, etc.: For various deductions under Chapter VIA.

- Schedule AMT: Computation of Alternate Minimum Tax (AMT) payable under Section 115JC.

- Schedule AMTC: Computation of tax credit under Section 115JD.

- Schedule SI: Statement of income taxable at special rates.

- Schedule IF: Information regarding partnership firms in which the firm is a partner (if applicable).

- Schedule PTI: Pass-Through Income details from business trusts or investment funds.

- Part B-TI: Computation of Total Income.

- Part B-TTI: Computation of Tax Liability on Total Income.

- Tax Payments: Details of Advance Tax, Self-Assessment Tax, and TDS/TCS.

- Verification: Declaration and verification section.

4. Review and Validate

- After filling in all the required details, carefully review all the information entered to avoid errors.

- The e-filing portal has a “Validate” option. Click on this to check for any missing mandatory fields or calculation errors. Correct any errors highlighted by the system.

5. Verification of the Return

Once the form is filled and validated, you need to verify the return. There are generally two primary ways for partnership firms to verify ITR-5:

Using Digital Signature Certificate (DSC):

- This is the mandatory method for firms whose accounts are liable to audit under Section 44AB.

- Ensure that the DSC of the designated partner (or authorized signatory) is registered and updated on the e-filing portal.

- Attach the DSC when prompted during the submission process.

Electronic Verification Code (EVC):

- If the firm is not liable for the audit, you might have the option to verify using EVC.

- EVC can be generated through various methods like Aadhaar OTP, Net Banking, Bank Account EVC, or Demat Account EVC.

- A code will be sent to the registered mobile number/email, which you need to enter to complete the verification.

6. Submit the Return

- Once the return is verified, click “Submit.”

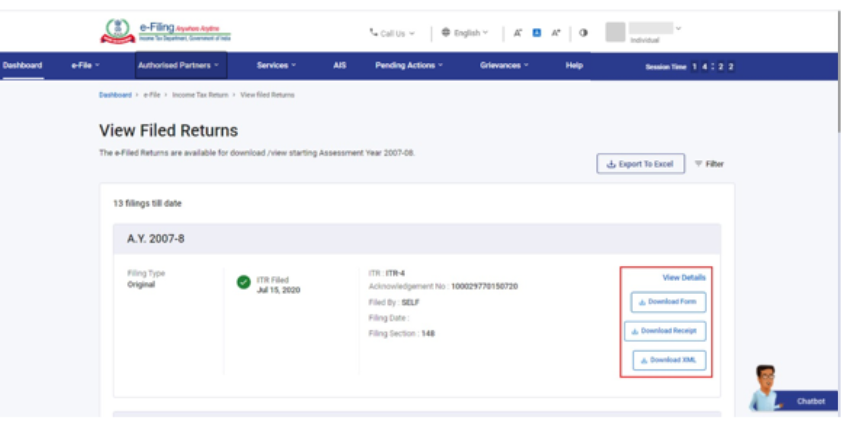

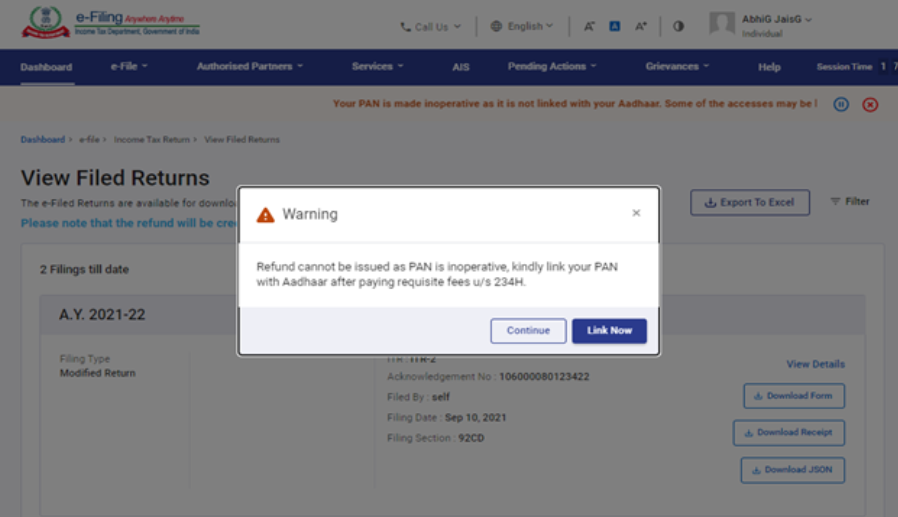

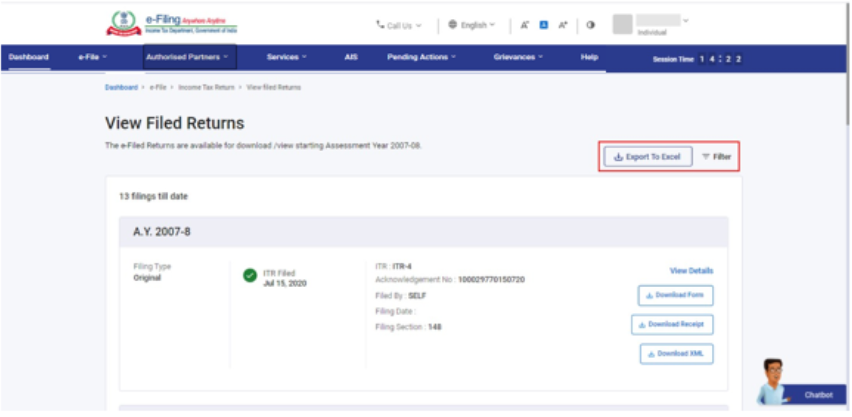

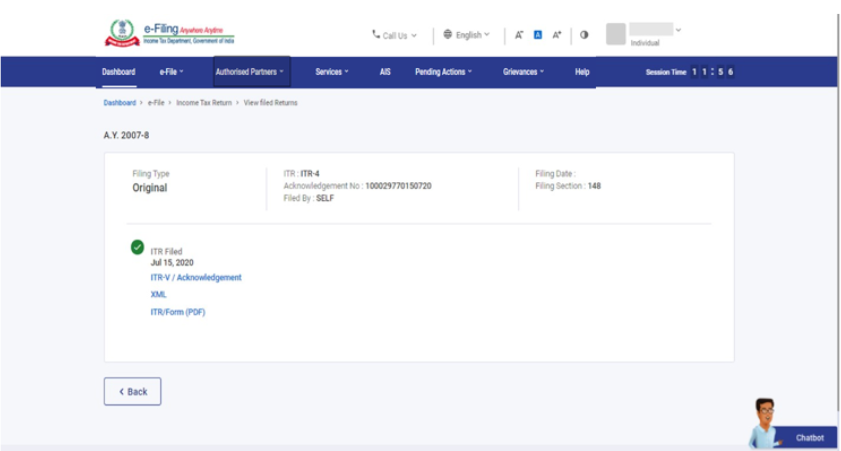

- Upon successful submission, an acknowledgement (ITR-V) will be generated.

- Download and save this ITR-V for your records. If you verified using DSC, your filing is complete.

7. Send ITR-V (if EVC was chosen and not completed online)

If you chose EVC but could not complete it online (or if you choose the “send ITR-V via post” option), you will need to print two copies of the ITR-V, sign one copy, and send it by ordinary post to:

- Centralized Processing Centre, Income Tax Department, Bengaluru – 560500, Karnataka.

This must be done within 30 days of filing the return. The other copy should be retained for your records. If the ITR-V is not received by CPC within 30 days, the return will be treated as not filed.