Trade License Online in India

Get your trade license approved without delays. RegisterKaro ensures your application meets all legal and municipal requirements for your shop, restaurant, factory, or commercial business from the start.

- Quick & Smooth Online Application Process

- Complete Documentation & Filing Support

- Expert Advice on License Type & Municipal Rules

- Assistance with Renewals, Updates & Compliance Checks

- Direct Coordination with Local Municipal Authorities

Enter your details to receive a full quote and consultation

By clicking, you consent to receiving updates about our services as outlined in our Privacy Statement.

4.6 out of 5

4.7 out of 5

What Sets Us Apart

500+ MCA Certified Experts

10,000+ Verified Reviews

2500+ Monthly Clients Onboardings

Serving Businesses Across India

What is Partnership Firm Registration?

Partnership firm registration is the legal process of establishing a business partnership under the Indian Partnership Act, 1932, with the Registrar of Firms. You need a minimum of two partners with no upper limit and zero minimum capital investment.

After you register a partnership firm, your business gains official legal status and benefits like partner protection, easier loan approvals, improved market reputation, and you operate with complete legal authority.

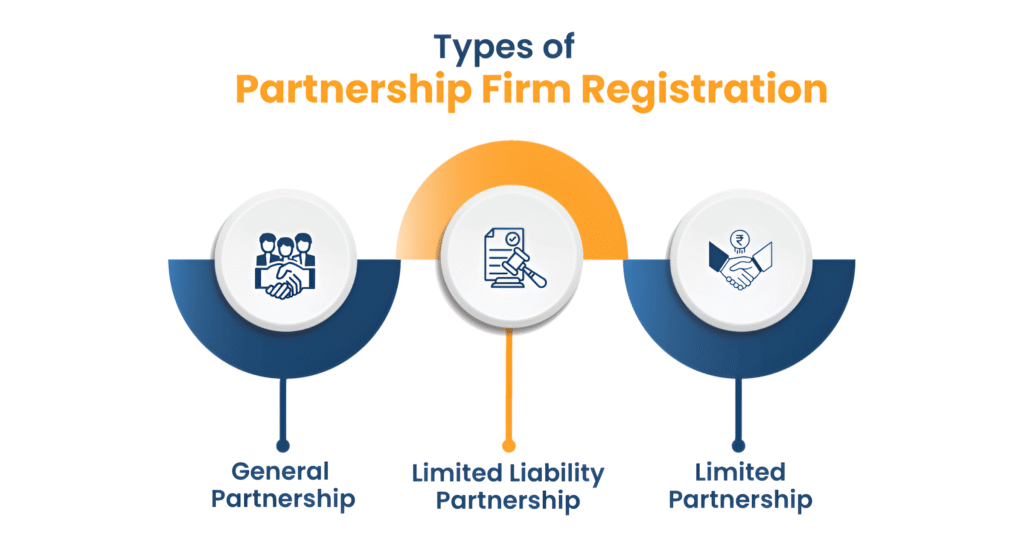

Types of Partnership Firms Eligible for Registration

The firm registration process covers different categories of partnerships:

- General Partnership: Traditional partnership where all partners share equal responsibility and liability for business operations and debts.

- Limited Liability Partnership (LLP): A hybrid structure combining the benefits of partnership and corporate entities with limited liability protection.

- Limited Partnership: A Structure where some partners have limited liability while others maintain unlimited liability.

Key Features of a Partnership Firm

A partnership brings together multiple people to run a business and share its rewards and risks.

- Two or More Partners: You need at least 2 people to start a partnership, with each person bringing money, skills, or work to the business.

- Shared Control: Every partner can make business decisions and sign contracts that legally bind the entire firm.

- Profit and Loss Sharing: Partners divide profits and losses according to their agreed percentage or split them equally.

- Personal Liability: If the business owes money, partners must pay from their own pockets if the business’s funds run out.

- No Legal Separation: The law sees the firm and its partners as the same – there’s no difference between them legally.

- Mutual Agreement: Partners join willingly and can end the partnership when they all agree to do so.

Purpose of Partnership Firm Registration

- Builds Legal Standing: Registration helps you enforce contracts and protect your rights.

- Improves Banking Access: Banks trust registered partnerships more and offer accounts and loans more easily.

- Tax Benefits: Registration gives you access to tax deductions and simpler tax filing procedures.

- Boosts Business Trust: Customers and suppliers prefer working with registered firms over informal partnerships.

- Simplifies Property Deals: Your firm can buy, sell, and own property directly in its name.

- Handles Disputes Better: Registered partnerships have clear legal ways to solve problems with partners or outsiders.

Laws Governing Partnership Firm Registration in India

Partnership firm registration in India is mainly governed by the following laws and regulations:

- Indian Partnership Act, 1932: This is the core law that regulates the formation, rights, duties, and dissolution of partnership firms. It defines how partners operate, share profits, and resolve disputes.

- Income Tax Act, 1961: It governs the taxation of partnership firms, including provisions for filing returns, calculating income, and paying applicable taxes.

- Goods and Services Tax (GST) Laws: A partnership firm must register for GST if its turnover exceeds the prescribed threshold for goods or services, and comply with all related tax obligations.

- Indian Contract Act, 1872: This law applies to the partnership agreement, ensuring the validity and enforceability of the partnership deed.

Regulatory Authorities

To legally register and run a partnership firm in India, you must coordinate with the following regulatory bodies:

- Registrar of Firms (RoF): The RoF in each state processes partnership firm registrations and maintains records under the Indian Partnership Act.

- Income Tax Department: This authority issues the PAN for the firm and oversees income tax compliance and filing.

- Goods and Services Tax Department: It manages GST registration and compliance if your turnover crosses the applicable limit.

- Local Municipal Authorities: You may also need to register your business under the Shops and Establishment Act, as per local laws.

These laws and authorities ensure that your partnership firm functions within the legal framework and fulfills all compliance requirements.

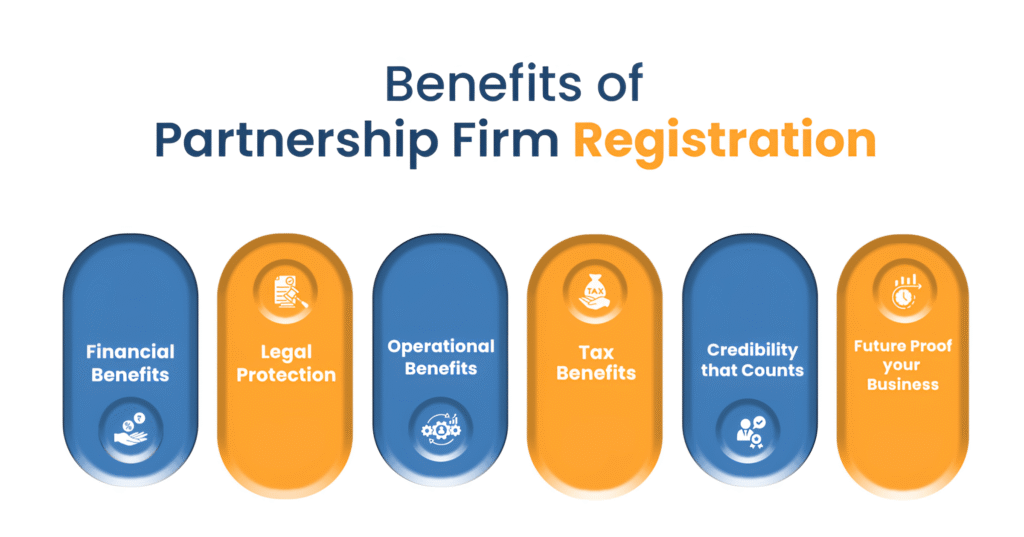

Benefits of Partnership Firm Registration

Registering a partnership firm in India provides several key advantages:

1. Legal Recognition & Protection

- Establish Legal Standing: Your partnership gains formal recognition, enabling partners to sue third parties and enforce business contracts effectively.

- Protect Business Identity: Registration provides legal proof of partnership existence and prevents disputes over business ownership.

2. Enhanced Credibility & Trust

- Establish Legal Standing: Your partnership gains formal recognition, enabling partners to sue third parties and enforce business contracts effectively.

- Protect Business Identity: Registration provides legal proof of partnership existence and prevents disputes over business ownership.

3. Financial Advantages

- Access Banking Services: Banks readily open current accounts and provide business loans to registered partnerships.

- Secure Credit Facilities: Financial institutions offer better credit terms and higher limits to registered firms.

4. Operational Benefits

- Resolve Partner Disputes: Clear partnership deed terms help settle internal conflicts and define roles effectively.

- Enable Business Expansion: Registration facilitates branch openings, franchise operations, and geographic expansion.

5. Tax Benefits

- Claim Business Deductions: Partners can claim legitimate business expenses and reduce overall tax liability.

- Access Government Schemes: Registered partnerships qualify for various MSME benefits, subsidies, and incentive programs.

6. Succession Planning

- Ensure Business Continuity: Formal partnership terms outline succession procedures and asset distribution methods.

- Facilitate Ownership Changes: Registration simplifies partner entry, exit, and ownership transfer processes.

Disadvantages of Partnership Firm Registration

However, registering as a partnership firm also has potential drawbacks to consider:

- Unlimited Personal Liability: Partners remain personally liable for all business debts and obligations without limitation.

- Joint and Several Liability: Each partner bears responsibility for actions and debts created by other partners.

- Limited Growth Potential: Partnerships cannot issue shares or raise capital through public offerings like companies.

- Restricted Ownership Transfer: Partners cannot freely transfer their interests without consent from other partners.

- Lack of Separate Legal Entity: The firm does not exist independently from its partners under law.

- Partnership Instability: Death, retirement, or withdrawal of any partner can dissolve the entire partnership.

- Management Disputes: Equal partnership rights can lead to deadlocks in decision-making processes.

Consulting with experienced legal and financial advisors helps navigate these challenges and structure partnerships effectively.

Eligibility Criteria for Partnership Firm Registration

To register a partnership firm in India, you must meet the following conditions:

- Include at least two partners: A minimum of 2 individuals must come together to form a partnership firm.

- Limit the number of partners to 50: The law allows up to 50 partners in a partnership firm.

- Prepare a written partnership agreement: You must draft and sign a partnership deed that clearly defines profit sharing, roles, and responsibilities.

- Set a lawful business objective: Your business must have a legal purpose and operate in compliance with Indian laws.

- Ensure only individuals act as partners: Only natural persons, not companies or legal entities, can become partners in a traditional partnership firm.

- Confirm all partners are adults: Every partner must be at least 18 years old and legally capable of entering into a contract.

- Submit valid identity and address proof: Each partner must provide government-issued ID and current address documentation.

- Avoid disqualified individuals: You must not include anyone declared insolvent, mentally unfit, or legally disqualified from managing a business.

By fulfilling these criteria, you can ensure a legally valid and properly structured partnership firm.

Documents Required for Partnership Firm Registration

To streamline the partnership firm registration process, make sure you have the following essential documents ready:

Essential Documents

- Partnership Deed: Draft a comprehensive partnership agreement that outlines the terms, roles, and responsibilities of all partners.

- PAN Cards of Partners: Each partner must submit a self-attested copy of their Permanent Account Number (PAN) card.

- Residential Address Proof: Submit valid address proof, such as an Aadhaar card, voter ID, or passport, for each partner.

- Business Address Proof: Provide documents that verify the address of your firm’s registered office.

- Photographs: Attach recent passport-size photos of all partners.

Additional Documents (if applicable)

- Rent Agreement: If the firm operates from rented premises, submit a copy of the rent agreement.

- NOC from Landlord: Obtain a No Objection Certificate from the property owner, granting permission to use the space for business purposes.

- Utility Bills: Provide the latest electricity or water bill for the business premises as address proof.

- Bank Statements: Submit recent bank statements of all partners as proof of financial identity.

Partnership Deed Requirements

Your partnership deed must include the following details:

- Full names and current addresses of all partners

- The nature and scope of the business

- Capital contribution made by each partner

- Agreed profit and loss sharing ratio

- Defined roles, rights, and duties of every partner

By submitting the correct documents and drafting a well-defined partnership deed, you can ensure a hassle-free registration process and avoid legal complications in the future.

Checklist for Partnership Firm Registration

✓ Finalize Partners & Name

✓ Draft Partnership Deed

✓ Stamp & Sign Deed

✓ Gather Partner Documents (PAN, Address Proofs)

✓ Arrange Business Address Proof

✓ Apply to Registrar (Optional but Recommended)

✓ Obtain a Firm PAN Card

✓ Open a Firm Bank Account

✓ Secure Other Licenses (GST, Shops & Establishment, etc.)

How to Register a Partnership Firm

Follow this step-by-step procedure to complete the registration of a partnership firm efficiently:

Step 1: Choose a Name for Your Partnership Firm

Pick a unique and relevant name that complies with state regulations. Make sure your chosen name:

- Reflects your business activities

- Doesn’t match existing registered firms in your state

- Avoids misleading or restricted words

- Doesn’t confuse the public or resemble a government body

Check name availability on your state’s Registrar of Firms portal. Since firm names are registered at the state level, similar names may exist in different states. Prepare two or three alternative names in case your first choice is unavailable or rejected.

Step 2: Draft the Partnership Deed

Prepare a detailed Partnership Deed that defines the structure and functioning of your firm. It should include:

- Names and full addresses of all partners

- Description of the business and its scope

- Each partner’s capital contribution

- Profit and loss sharing ratio

- Duties, responsibilities, and rights of each partner

- Duration of the partnership (if applicable)

- Rules for admitting new partners or handling partner exits

Sign the deed on non-judicial stamp paper of appropriate value (as per your state’s rules). All partners must sign the document in the presence of witnesses. Notarize the deed to enhance its legal validity.

Step 3: You Obtain a PAN Card for the Firm

After you and your partners execute the partnership deed, you must apply for a Permanent Account Number (PAN) card in the partnership firm’s name. The firm mandatorily needs this for tax purposes and to open a bank account. You can complete this application online through the NSDL or UTIITSL websites.

Step 4: You Fill Out the Application for Registration (Form No. 1)

You can obtain Form No. 1 (the application for registering a partnership firm) through the official website of the Registrar of Firms (RoF) in your respective state. In this application form, you provide details such as:

- The firm name.

- The nature of your business.

- The main location of your firm’s business.

- The full names and permanent addresses of all partners.

- The date each partner joined the firm.

- The duration of the firm.

All partners, or their authorized agents, must sign this application.

Step 5: You Submit Documents to the Registrar of Firms

Along with the application form, you generally submit the following documents:

- The original Partnership Deed, correctly signed, notarized, and on appropriate stamp paper.

- The required registration fee (this fee differs by state).

- A copy of the firm’s PAN card.

- Address proof for the firm’s main place of business (like a rent agreement or utility bill).

- PAN cards and address proofs (such as Aadhaar card, voter ID, or passport) for all partners.

- An affidavit in which you declare that all the details you provided in the application and documents are correct.

Step 6: Receive Your Registration Certificate

After successful verification, the Registrar of Firms will issue a Certificate of Registration with a unique firm number. This Certificate is your legal proof for registration.

Step 7: Open a Current Bank Account for the Firm

Once the firm’s registration is complete and you have the Certificate of Registration and the firm’s PAN card, you can open a current bank account in the partnership firm’s name. You need this account to manage the firm’s finances.

Note: Different states in India may have varying procedures, forms, fees, and stamp duty for partnership firm registration, as allowed under the Indian Partnership Act, 1932. It’s advisable to consult a legal expert to ensure accurate drafting of the partnership deed.

Fees and Penalties of Partnership Firm Registration

The registration fees of a partnership firm and the penalties for non-compliance are:

Registration Costs

The cost of partnership firm registration involves several components:

| Fee Category | Item | Cost/Range |

|---|---|---|

| Government Fees | ||

| Partnership deed stamp duty | 200 to 2,000 (varies by state and capital) | |

| Registration fees | 200 to 1,000 (varies by state) | |

| Name search and reservation | 100 to 500 | |

| Professional Fees | ||

| Partnership deed drafting | 3,000 to 8,000 | |

| Legal consultation | 2,000 to 5,000 | |

| Registration assistance | 5,000 to 15,000 | |

| Post-Registration Costs | ||

| PAN card application | 110 (online) / 225 (physical) | |

| TAN registration | Free online | |

| Bank account opening | Varies by bank | |

| GST registration (if applicable) | Free + Professional charges (if any) | |

Penalties for Non-Compliance

Failing to meet regulatory requirements can result in significant penalties:

| Non-Compliance / Default | Form (if applicable) | Penalty Details |

|---|---|---|

| Operating without registration | N/A | Partners lose the right to sue third parties for business disputes. |

| Failure to file Income Tax Returns | ITR-5 | Rs 5,000 (if income up to Rs 5 lakh), Rs 10,000 (if income above Rs 5 lakh). |

| Late GST return filing | GSTR-1, GSTR-3B | Rs 200 per day per return (minimum Rs 500). |

| Non-maintenance of books of accounts | N/A | Penalty up to Rs 25,000 under the Income Tax Act. |

| Failure to deduct TDS | Form 26Q, 24Q | 1% per month or part thereof on the TDS amount. |

| Non-compliance with labor laws | Various | Rs 10,000 to Rs 1 lakh, depending on the violation. |

| Violation of partnership deed terms | N/A | Internal disputes and potential dissolution. |

Cancellation of Registration of Partnership Firm

The registration of a partnership firm can be cancelled in the following two primary ways:

- Automatic Cancellation: Certain events automatically trigger the end of the firm’s registration:

- Partnership Dissolves: If the partners dissolve the partnership itself, as outlined in their agreement or by law, the registration can automatically terminate.

- Firm Converts: When partners choose to change their business structure, for instance, by converting the partnership into a company, the original partnership registration ends.

- Firm Fails to Comply: If the partnership does not follow key government regulations, authorities can cancel its registration.

- Voluntary Cancellation: Partners can choose to end the firm’s registration:

- Partners Mutually Agree: All partners can decide together to close the business and cancel its registration.

- Business Shuts Down: When partners permanently close the business, they typically apply to cancel the registration.

- Firm Merges: If the partnership merges with another business, the partners usually cancel their existing registration as part of that process.

Renewal of Partnership Firm Registration

Once you register your partnership firm, that registration is generally considered permanent. This means there is a need for renewal of partnership firm registration in future years.

Post Registration Compliance Requirements for a Partnership Firm

After registration, partnership firms in India must fulfill various tax, regulatory, and documentation-related obligations to remain legally compliant.

1. Income Tax Filing

Partnership firms must file Income Tax Returns annually using Form ITR-5.

- The due date is 31st July for non-audited firms and 31st October if an audit is required.

- Tax audit becomes mandatory if turnover exceeds ₹1 crore for businesses or ₹50 lakh for professionals.

2. Tax Deducted at Source (TDS)

If the firm is liable to deduct TDS (e.g., salary, contractor payments), it must:

- Deduct and deposit TDS on time.

- Quarterly TDS returns filing.

- Issue TDS certificates to payees.

3. GST Compliance (If Registered)

Firms registered under GST must:

- File monthly or quarterly GSTR-1 and GSTR-3.

- Annual GST return filing (if applicable).

- Maintain GST-compliant invoices and records.

- Generate e-way bills for applicable goods transport.

4. Partnership Deed Amendments

Any change in partnership (addition/removal of partner, capital change, etc.) requires:

- An updated deed.

- Re-registration (if the firm is registered) with the state’s Registrar of Firms.

5. Maintenance of Books and Accounts

Maintain proper books of accounts, including:

- Cash book, ledger, and bills.

- Profit and loss account and balance sheet.

- Partner capital accounts.

6. Compliance with State-Specific Laws

Firms operating in commercial establishments must do Shops and Establishments Act registration applicable in their state and renew it as required.

7. Other Applicable Licenses

Depending on business activity, the firm may need:

- FSSAI license (for food business).

- Professional tax registration.

- A Trade license from the local authority.

These compliances help the firm stay legally valid, financially transparent, and ready for audits or funding.

Partnership Firm Registration Certificate

This certificate is proof that your partnership firm exists in the eyes of the law. It gives your firm official legal recognition under the Indian Partnership Act. It authorizes to opening of a bank account in the firm’s name, legal status to enter into contracts, and conduct business transactions.

If you feel a partnership might not be the best fit for your business, you can also complete your company registration online to set up other types of business entities easily.

Connect with RegisterKaro and let our experts handle the legal hassle while you grow your business.

Frequently Asked Questions (FAQs)

How to get a trade license?

You can get a trade license by applying to your local Municipal Corporation. This can be done either online through the municipality’s official website or offline by visiting the licensing department office in person.

How to apply trade license online in India?

To apply online, visit your city’s municipal corporation portal, create a user account, fill out the new trade license application form, upload scanned copies of required documents, pay the fee online, and submit the application.

What is the cost of a trade license in India?

The cost varies widely depending on the state, city, business type, and size of your premises. It can range from ₹500 for a small shop to over ₹10,000 for larger establishments.

What are the documents required for a trade license?

Key documents include identity and address proof of the owner(s), proof of the business’s legal structure (e.g., incorporation certificate for a company), and proof of the business premises (e.g., rent agreement or property tax receipt).

How to renew a trade license online?

To renew online, log in to the municipal portal, select the “Renew Trade License” option, enter your existing license number, verify the auto-filled details, upload any required documents like the latest tax receipt, and pay the renewal fee online.

What is the penalty for not renewing the trade license?

Failure to renew your license on time results in late fees, which are often charged daily or monthly. Operating with an expired license can lead to heavy fines or even the closure of your business by authorities.

What is the duration of time required to get a trade license certificate?

In metropolitan cities, it usually takes 7 to 15 working days after application submission and fee payment. In smaller towns or rural areas, it can take up to 30 days.

Is a trade license mandatory for an online business?

Yes, it is generally mandatory if your online business has a physical presence, such as an office, a warehouse for storing goods, or a packaging facility. The law applies to the premises where you operate.

Is a trade license mandatory for GST registration?

While they are separate registrations, they are practically linked. Many banks require a Trade License to open a business current account, which is necessary for GST registration. Also, the GST registration process may ask for proof of a legally established place of business, for which a Trade License can serve as evidence.

Who is eligible for a trade license in India?

Any individual who is 18 years or older, has no criminal record, and is running a legally permissible business is eligible to apply.

How many types of trade licenses are there?

There are primarily three types: Industrial License (for manufacturing), Shop/Commercial License (for trading and services), and Food Establishment License (for food-related businesses). There are also miscellaneous licenses for other specific trades.

How to cancel a trade license?

To cancel your license, you must submit a formal application for closure to the municipal corporation. You will need to surrender the original license certificate and provide proof that the business has been closed.

How to find the trade license number?

Your unique Trade License Number is printed on the trade license certificate issued to you by the municipal authority.

Are commercial license and trade license the same?

In the Indian context, a “commercial license” is generally considered a type or category of a trade license (for commercial trading activities) and not a separate, distinct license.

Is a trade license required for a private limited company & proprietorship?

Yes, a trade license is mandatory for both a private limited company and a sole proprietorship if their business activities fall under the regulations of the local municipal corporation where they operate.

Why Choose Registerkaro for a Trade License?

When you choose RegisterKaro, you get everything you need to secure your trade license quickly and legally.

- Clear Guidance on License Requirements: Expert consultation to identify the exact type of trade license your business needs based on its nature and location.

- Well-Organized Documentation: Get help preparing and organizing all necessary documents, reducing the chances of errors or rejections.

- Complete Filing Support: Your application is professionally filed with the local municipal authority, accurately and on time.

- Application Tracking & Follow-up: Regular updates as your application moves through the approval process, with dedicated follow-ups handled for you.

- Peace of Mind & Legal Compliance: Confidence in running your business legally, with ongoing support for renewals and compliance when needed.

Trade License in State

Trade License in Andhra Pradesh

Trade License in Assam

Trade License in Bihar

Trade License in Goa

Trade License in Gujarat

Trade License in Haryana

Trade License in Jharkhand

Trade License in Karnataka

Trade License in Kerala

Trade License in City

Trade License in Visakhapatnam

Trade License in Guwahati

Trade License in Gurgaon

Trade License in Ranchi

Trade License in Bangalore

Trade License in Mysore

Trade License in Bhopal

Trade License in Mumbai

Trade License in Pune

What Our Clients Say

S

Sanket Chawre

- Verified

Others

We had been struggling with many things during our LLP setup with RegisterKaro until Sonal stepped in as our compliance officer and overall liason. So…

Date Posted

2025-12-23

A

Ayusha Kumar

- Verified

Others

I had a great experience getting my company incorporated with the help of Ms. Anchal Gupta. She managed the entire process very efficiently and profes…

Date Posted

2025-12-23

P

Pradip Vernekar

- Verified

Others

I had an excellent experience with RegisterKaro. Atisha Jain and the team made the process of getting my GST certificate seamless and hassle-free. The…

Date Posted

2025-12-23

D

Dhariya

- Verified

Others

I recently had a great experience with RegisterKaro and their employee, Satyapriya Tripathi. They provided exceptional assistance with my professional…

Date Posted

2025-12-23

Latest Blogs

January 14,2026

What are CDSCO Guidelines for Medical Devices?

Joel Dsouza

Learn about CDSCO guidelines for medical devices in India. This guide covers classification, approval process, and compliance for manufacturers & importers.

January 14,2026

What are the Documents Required for a Trade License?

Srihari Dhondalay

Learn about the documents required for a trade license in India. This checklist covers key requirements, forms, renewal documents, and specific cases.

January 14,2026

How to Download the FSSAI Certificate Online? 2026 Guide

Joel Dsouza

Learn how to download an FSSAI certificate online using FOSCOS. This guide covers the process, license number method, and registration certificate steps.

January 14,2026

How to Get a Trade License for a Dental Clinic?

Srihari Dhondalay

Learn how to get a trade license for a dental clinic in India. Know the eligibility, process, and documents needed for clinic license registration.

January 14,2026

What is a Trade License? Eligibility, Types & Process

Joel Dsouza

Learn what a trade license is in India, its purpose, and key types. This article covers eligibility, fees, and the complete process to apply easily.

January 14,2026

Why is CDSCO Form 44 Important for New Drug Approval?

Joel Dsouza

Learn why CDSCO Form 44 is crucial for new drug approval in India. Explore its checklist, process, and documents needed for filing Form 44 with CDSCO.

Featured In